2. THE PAYCHECK PROTECTION PROGRAM

Article overview:

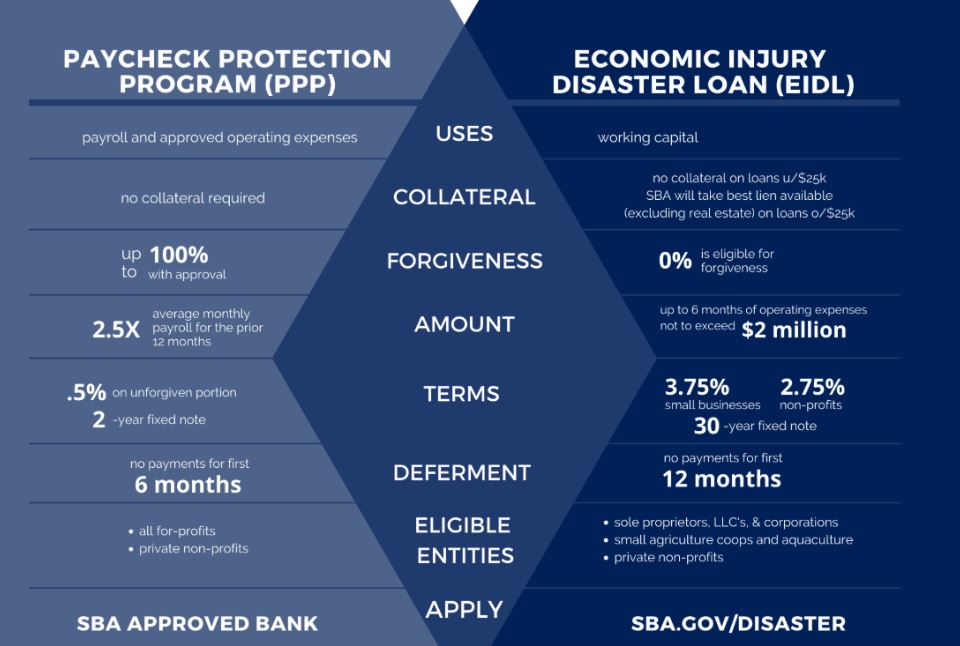

- Small businesses can apply for 100% guaranteed loans of up to $10 million to help keep workers employed.

- Interest rate of 0.5%

- Maturity of 2 years

- First payment deferred for six months

- 100% guarantee by SBA

- No collateral

- No personal guarantees

- No borrower or lender fees payable to SBA

Paycheck/Payroll Protection Program is part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which consists of $349 billion in government-backed forgivable loans to help small businesses continue paying payroll costs and certain operating expenses for up to eight weeks. This is a federal first-come, first-serve basis program so apply ASAP.

Small businesses may each be eligible for up to $10 million to cover payroll and other employee benefits (PTO, insurance premiums, retirement, etc.). The loan may also be used to pay interest on mortgages, rent, and utilities

How much does your small business qualify for? 2.5 times your business average monthly payroll costs with no more than $10 million. Payroll costs are capped at $100,000 on an annualized basis for each employee.

However, SBA and banks are still debating on the most accurate calculation method to use.

Loan payments are deferred for six months.

What is the interest rate? 0.5% fixed rate

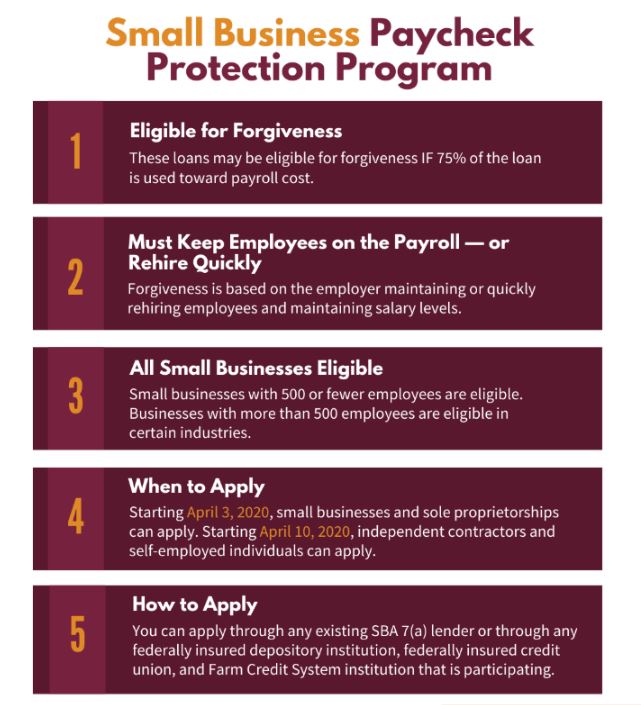

Are Paycheck Protection Program loans fully forgiven? Funds are provided in the form of loans that will be fully forgiven when used for payroll costs, interest on mortgages, rent, and utilities (due to likely high subscription, at least 75% of the forgiven amount must have been used for payroll).

Loan payments will also be deferred for 6 months. No collateral or personal guarantees are required.

Neither the government nor lenders will charge small businesses any fees.

How can I request loan forgiveness?

You can submit a request to the lender that is servicing the loan. The request will include documents that verify the number of full-time equivalent employees and pay rates, as well as the payments on eligible mortgage, lease, and utility obligations.

You must certify that the documents are true and that you used the forgiveness amount to keep employees and make eligible mortgage interest, rent, and utility payments.

The lender must make a decision on the forgiveness within 60 days.

Must small businesses keep employees on payroll or rehire quickly? Yes.

Forgiveness is based on the employer maintaining or quickly rehiring employees and maintaining salary levels. Forgiveness will be reduced if full-time headcount declines, or if salaries and wages decrease.

Re-hiring requirements are? Employers have until June 30th, 2020 to restore full-time employment and salary levels for any changes made between February 15th and April 26th 2020.

Which small businesses are eligible? Small businesses with 500 or fewer employees—including nonprofits – churches, veteran organizations, tribal concerns, self-employed individuals, sole proprietorships, and independent contractors are eligible. Businesses with more than 500 employees are eligible in certain industries.

To be eligible special rules apply to the following businesses: accommodation, restaurants/food services, gig economy workers and franchises.

Which counts as payroll costs?

- Salary, wages, commissions, or tips.

- Employee benefits including costs for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payments required for the provisions of group health care benefits including insurance premiums; and payment of any retirement benefit;

- State and local taxes assessed on compensation; and

- For a sole proprietor or independent contractor: wages, commissions, income, or net earnings from self-employment, capped at $100,000 on an annualized basis for each employee.

Do I need to personally guarantee this loan? No. There is no personal guarantee or collateral requirement.

However, if the proceeds are used for fraudulent purposes, the Federal government will pursue criminal charges against you.

When should I apply?

- Starting April 3, 2020, small businesses and sole proprietorship’s can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders.

- Starting April 10, 2020, independent contractors and self-employed individuals can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders.

How do I apply?

You can apply through any existing SBA 7(a) lender or through any federally insured depository

Institutions, federally insured credit union, and farm credit system institution that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. Online application and document submittal is available for these federally insured depository institutions: Wells Fargo, Bank of America, US Bank, Heritage PNC Bank, Fifth-Third, Fountainhead, Chase Bank. Also check out this SBA Participating Lenders List.

All loans will have the same terms regardless of lender or borrower.

The Paycheck/Payroll Protection Program is implemented by the Small Business Administration with support from the Department of the Treasury to help small businesses.

Application forms are available here: https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Application-3-30-2020-v3.pdf

To learn more about the Paycheck Protection Program, contact your preferred lender and visit: https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/paycheck-protection-program-ppp

#PaycheckProtectionProgram #PayrollProtectionProgram #PPE #SBA